TIL Limited (NSE: TIL), India’s leading material handling and infrastructure equipment manufacturer, today announced its Q4FY26 and full year FY26 financial results. The year marks a decisive strategic transition in TIL’s performance trajectory — While FY26 profitability remained impacted by financing costs, currency pressure, and one-time settlement expenses, core machine sales and operational execution improved materially during H2, and the company closed FY26 with a board-approved acquisition that opens a new clean energy manufacturing vertical.

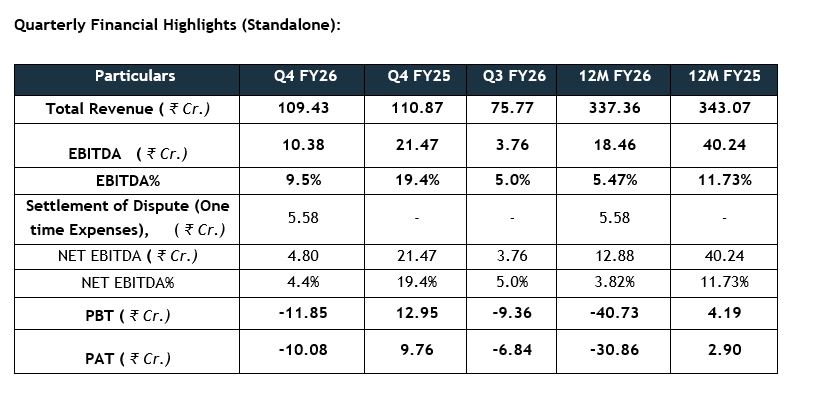

Overall revenue for FY26 stood at ₹337.36 Cr, reflecting a nominal decrease compared to ₹343.07 Cr in FY25. This reduction was driven primarily by a substantial decline in other income — from ₹27.79 Cr in FY24-25 to ₹14.11 Cr in FY25-26, a reduction of approximately 49% — attributable to lower non-operational income, while core operations remained relatively strong. Machine sales, the primary measure of operational health, grew 4% year-on-year to ₹265.33 Cr, reflecting the growing commercial momentum of TIL’s expanded product portfolio and improving order execution capability.

Some large orders won during the year included the ₹66.75 Cr CONCOR contract for 25 loaded ReachStackers, approximately ₹110 Cr in orders from the Indian Army and Indian Air Force for approximately 170 military cranes, and a large ₹30+ Cr Operation and Maintenance contract from CONCOR — marking TIL’s re-entry into the high-margin services segment and strengthening recurring income visibility and deepening customer engagement beyond equipment supply. Three newly commercialised indigenous products — spanning the pick and carry, truck crane, and rough terrain equipment segments — moved from their EXCON 2025 market debut to active field trials and customer engagements during Q4, with enquiry conversions sustaining into FY27.

The year also marked the company’s landmark entry into the clean energy space with the board’s approval for majority stake acquisition in Tulip Compression Private Limited (TCPL). The acquisition was concluded in May 2026 and will now give TIL access to LNG and Hydrogen powerpacks and opens specialised manufacturing markets across CNG, LNG, and Hydrogen equipment, large-scale cryogenic LNG storage, and oil and gas process vessels.

The company also made measurable progress on material efficiency — raw material cost ratio improved from 64.5% in FY24-25 to 63.9% in FY25-26, an early but meaningful indicator of better sourcing discipline, pricing rigour, and product mix optimisation. The true impact of this improvement is expected to reflect in FY27 as and when global supply chains stabilise. Employee costs and operational costs saw a slight increase, reflecting the company’s conscious investment in building skilled and trained manpower essential to support its product expansion and growth ambitions for the future. The company also resolved legacy taxation-related disputes on account of entry tax through Settlement of Disputes (SOD, One Time), extinguishing a contingent liability of ₹23.12 Cr and VAT/CST related disputes, reducing another contingent liability of ₹21.68 Cr, bringing closure to long-pending cases and strengthening the balance sheet for the future.

Commenting on the results, Mr Alok Kumar Tripathi, President & Whole Time Director, TIL Limited, said, “TIL is gradually becoming a defence mobility manufacturer, a lifecycle infrastructure partner, a clean-energy engineering platform and an indigenous heavy-equipment company. In FY25-26, TIL has demonstrated recovery in core machine sales, operational performance and shown financial resilience in H2 and Q4 despite four major challenges. The first two were global geopolitical uncertainties and supply-chain disruptions that mellowed our topline, and the latter were a weakening rupee and rising freight costs that directly impacted material cost and took a bite out of our bottom line. Despite this, the company has maintained a positive EBITDA despite substantial financing costs, lower other income, and one-time SOD expenses.”

Mr. Pinaki Niyogy, CTO & CGO, TIL Limited, added: “TIL is evolving from a cyclical equipment company into a broader engineering platform. Our new indigenous products have been well received across retail and defence verticals and we will soon commercialise them along with a few newer platforms. We are also extending our heavy engineering capability into India’s clean energy and gas infrastructure sector with Tulip Compression joining the TIL family. TIL’s core strength remains its indigenous engineering capability, which offers a powerful import substitution opportunity and will help build a truly Atmanirbhar Bharat.”

Mr. Pinaki Niyogy, CTO & CGO, TIL Limited, added: “TIL is evolving from a cyclical equipment company into a broader engineering platform. Our new indigenous products have been well received across retail and defence verticals and we will soon commercialise them along with a few newer platforms. We are also extending our heavy engineering capability into India’s clean energy and gas infrastructure sector with Tulip Compression joining the TIL family. TIL’s core strength remains its indigenous engineering capability, which offers a powerful import substitution opportunity and will help build a truly Atmanirbhar Bharat.”

TIL enters FY27 as a more diversified, capable, and forward-looking organisation with a ₹274 Cr order pipeline, a strengthened net worth, new indigenous products in various stages of development and a re-entry into high-value recurring O&M revenues. As India accelerates development, TIL is rebuilding itself as an Indian industrial engineering platform aligned to three national priorities of infrastructure, defence indigenisation and energy transition.